RGM are proud to announce that financial advisory firm Money Talk Planners will be joining forces with RGM come the 1st of July 2025.

Money Talk Planners is a locally, family-owned financial planning business based out of Morwell that has been in operation for over 30 years. It has a reputation of providing high quality advice to its clients in a professional manner; values that underpin the services we provide at RGM. With the move, the entire Money Talk Planners team will reside in our Traralgon office.

There will be no change to the existing service provided to all our financial planning and accounting clients. Joe Auciello, Partner of over ten years in both our accounting and financial planning divisions, explains why RGM sought out this alliance. “In the ever-growing financial advisory sector, it is imperative that as a business, we look at strategic moves to ensure we can bolster our service offering to existing and new clientele. The Money Talk Planners team will bring their own ideas across to RGM that we look forward to incorporating into our business. Over the past two years we have been diligently working in the background to ensure that this move puts RGM at the forefront of financial planning in Gippsland both now and into the future”.

As part of the move, MTP practice principal Tony Salvatore and financial advisor Adrian Salvatore will join the ownership group of RGM. With over 30 years of financial of financial planning experience, Tony is excited about the move. “Both businesses have shared values, and we will be able to offer enhanced resources, greater financial guidance and invest quality time with our clients. It will be business as usual.”

We formally welcome the Money Talk Planning team across to RGM and we’re all excited in what the future holds!

The number of Australians aged over 65 is expected to more than double in the next 40 years while the number of people aged over 85 is predicted to triple in that time.i

Aged care funding and services have seen major changes in the years since the 2021 report of the Royal Commission into Aged Care Quality and Safety, and this year is no exception.

1 July 2025 marks the start of a host of new programs and improvements for the aged care sector. Several announcements have already been made this year, covering wage rises for aged care workers and nurses, and an increase in government funding for residential aged care accommodation.

In one of the most significant changes, the new Aged Care Act begins on 1 July. The Act aims to ensure the viability and quality of aged care.

A report by the Aged Care Taskforce last year calculated the residential aged care sector will need $56 billion by 2050 to upgrade facilities and build more rooms.

Current funding arrangements aren’t working. In the 2022-2023 financial year, almost half of all accommodation providers made a loss.

Some $300 million in federal grants will be delivered to accommodation providers this year to help with capital works upgrades.

And to improve the viability of the facilities the government is introducing other measures including larger means-tested contributions from new entrants and a higher maximum room price that is indexed over time.

Aged Care Minister Anika Wells says half of new residents will not contribute more under the new consumer contributions.

“For every $1 an older Australian contributes to their residential aged care, the government will contribute an average of $3.30,” says Wells.

Support at Home

The Aged Care Act also aims to support more people who want to stay in their own homes as they age. The federal government is investing $4.3 billion in a new Support at Home program, which replaces the Home Care Packages and the Short-Term Restorative Care programs.ii

There’ll be more than 300,000 places available over the next 10 years and a shorter waiting period for Support at Home, and there’s a goal to simplify and improve the assessment process, making it easier to access different services as needs change.iii

Similar to the Home Care Package, Support at Home will provide:

clinical care, such as nursing and occupational therapy,

help with maintaining independence including showering, dressing and taking medications, and

support for everyday living tasks such as cleaning, gardening, shopping and meal preparation.

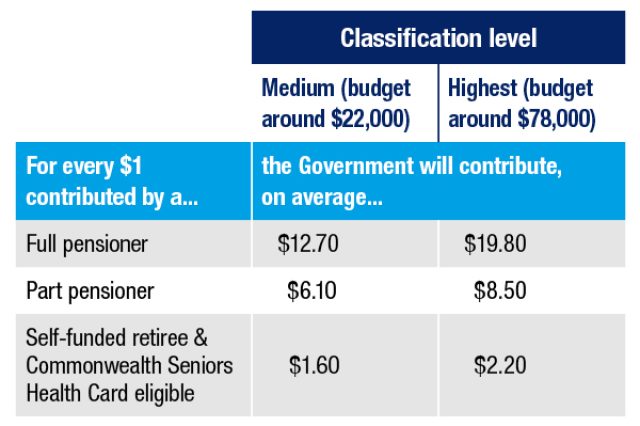

The government will pay 100 per cent of clinical care costs while Support at Home recipients will make a contribution towards independence and everyday living costs. The contribution amount will be calculated using the Age Pension means test and it depends on the level of support needed and the combination of income and assets. The highest classification with the most funding will receive a package of services worth $78,000 per year. There’ll also be funding for assistive technology and home modifications and end of life care.

A new cap on contributions will also apply. No one will pay more than $130,000 in their lifetime – whatever their means or length of care at home or in residential accommodation.

Refunding deposits

The new Aged Care Act also requires aged care accommodation providers to refund residents’ lump sum deposits within 14 days if they move to another facility or pass away. Interest must be paid on the lump sum until the amount is repaid. As before, some deductions are permitted provided they were included in the original agreement.

No disadvantage

For those already receiving home care packages or in aged care accommodation, the government says a ‘no-worse-off’ principle will provide certainty that they won’t have to pay more under the new laws.

Whether it is you or a loved one who is considering moving into aged care, it can be an emotional time. With these new changes being implemented, you may have a few questions. Please give us a call if you’d like to hear more about the changes or if we can help to assess your next step or plan ahead.

In the shadow of an upcoming election, Jim Chalmers’ fourth Budget delivered small but unexpected tax cuts for all Australian taxpayers.

The modest cuts were delivered against a backdrop of growing economic uncertainty, with the treasurer emphasising the need for national resilience in the face of rapid global change.

Tax cuts for everyone

In a surprise revelation, the treasurer announced two new tax cuts in the 2025 Budget.

The first is a cut in the lowest personal income tax rate, which covers every dollar of a taxpayer’s income between $18,201 and $45,000. The current 16 per cent rate will reduce to 15 per cent in 2026-27 and be lowered again to 14 per cent from 1 July 2027.

According to the government, the reduction will take the first tax rate down to its lowest level in more than half a century. Combined with the 2024 tax cuts, an average earner will be paying $2,190 less in 2027-28 compared with 2023-24.

The second tax cut is an increase of 4.7 per cent to the Medicare low-income threshold for singles and families. This means the Medicare Levy will not kick in until singles earn $27,222, rather than the current $26,000 level. The threshold for families will rise from $43,846 to $45,907, while single seniors and pensioners will have their threshold increase from $41,089 to $43,020.

Energy relief for small business and households

The Budget also provided small businesses and households with a welcome additional energy bill rebate to cope with the burden of high energy costs.

Around one million eligible small businesses will receive an additional $150 directly off their energy bills from 1 July 2025. This will extend the government’s energy bill relief until the end of 2025, as the previous rebate scheme was due to end on 30 June.

Abolition of non-compete clauses and licensing reform

Some businesses may be less pleased with the Budget announcement of a planned ban on non-compete clauses covering low- and middle-income employees leaving for another business or to start their own.

Competition law will be tightened to prevent businesses making arrangements that cap workers’ pay and conditions without their knowledge or agreement, or that block them from being hired by competitors. The government claims this will increase affected employees’ wages by up to 4 per cent as they will be able to move to more productive, higher-paying jobs.

Work will also begin on a national occupational licence for electrical trades, which is intended to provide a template for other industries where employees are currently restricted from working across state and territory borders.

Beer excise freeze

Government support for the hospitality sector and alcohol producers was also announced in the Budget.

Indexation of the draught beer excise and excise equivalent customs duty rates will be paused in a measure costing about $165 million over five years.

Strengthening competition law

Small business will benefit from the government’s decision to work with the states and territories to extending unfair trading practices protections to small businesses.

Over $7 million will be provided over two years to strengthen the Australian Competition and Consumer Commission’s enforcement of the Franchising Code.

Subject to consultation, protections from unfair contract terms and unfair trading practices will be extended to all businesses regulated by the Franchising Code.

Supporting Australian businesses

Local companies will also benefit from $20 million in additional support for the Buy Australian Campaign, which encourages consumers to buy Australian-made products.

The Budget further supported local businesses with $16 million in funding for a new Australia-India Trade and Investment Accelerator Fund.

Additional ATO tax compliance funding

The ATO will be happy, with the 2025 Budget providing $999 million over the next four years to extend and expand its tax compliance activities.

This includes additional funding for the shadow economy and personal income tax compliance programs, together with $50 million from 1 July 2026 to ensure the timely payment of tax and unpaid super liabilities by businesses and wealthy groups.

Deciding when to retire is a big decision and even more difficult if you are concerned about your retirement income.

The average age of Australia’s 4.2 million retirees is 56.9 years but many people leave it a little later to finish work with most intending to retire at just over 65 years.i

If you’re not quite ready to retire, a ‘transition to retirement’ (TTR) strategy might work for you. It allows you to ease into retirement by:

supplementing your income if you reduce your work hours, or

boosting your super and save on tax while you keep working full time

The strategy allows you to access your super without having to fully retire and it is available to anyone 60 years or over who is still working.

Working less for similar income

The strategy involves moving part of your super balance into a special super fund account that provides an income stream. From this account you can withdraw funds of up to 10 per cent of your balance each year.

As you will still be earning an income and making concessional (before-tax) contributions to your super, this approach allows you to maintain income during the transition to full retirement while still increasing your super balance, as long as the contributions continue.

Note that, generally speaking, you can’t take your super benefits as a lump sum cash payment while you’re still working, you must take super benefits as regular payments. Although, there are some exceptions for special circumstances.

Take the example of Alisha.ii Alisha has just turned 60 and currently earns $50,000 a year before tax. She decides to ease into retirement by reducing her work to three days a week.

This means her income will drop to $30,000. Alisha transfers $155,000 of her super to a transition to retirement pension and withdraws $9,000 each year, tax-free. This replaces some of her lost pay.

Income received from your super fund under a TTR strategy is tax-free but note that it may affect any government benefits received by your or your partner.

Also, check on any life insurance cover you have under with your super fund in case a TTR strategy reduces or stops it.

Give your super a boost

For those planning to continue working full-time beyond age 60, a TTR strategy can be used to increase your income or to give your super a boost.

To make it work, you could consider increasing salary sacrifice contributions into your super then using a TTR income stream out of your super fund to replace the cash you’re missing from salary sacrificing.

In another example, Kyle is 60 and earns $100,000 a year. He intends to keep working full-time for at least another five years. Kyle transfers $200,000 from his super to an account-based pension so he can start a TTR strategy then salary sacrifices into his super.

This will reduce his income tax, but also his take-home pay. So, he tops up his income by withdrawing up to 10 per cent of his TTR pension balance each year.iii

A TTR strategy tends to work better for those with a larger super balance, a higher marginal income tax rate and those who have not reached the cap on concessional contributions.

Nonetheless, it can still be useful for those with lower super balances and on lower incomes, but the benefits may not be as great.

Some things to think about

TTR won’t suit everyone. For example, be aware that you cannot withdraw more than 10 per cent of your super balance each year.

Also, if you start withdrawing your super early, you will have less money when you retire.

The rules for a TTR strategy can be complex, particularly if your employment situation changes or you have other complicated financial arrangements and investments. So, it’s important to seek professional advice to make sure it works for you and that you are making the most of its benefits.

If you would like to discuss your retirement income options, give us a call.

Achieving your long-term financial goals doesn’t need to be overwhelming. If you can put in place some basic financial steps, you are on the road to a successful outcome.

It means keeping on top of your options and devising strategies for investment, debt reduction and risk protection. The start of the year is a perfect time to take a few proactive steps, that your future self will thank you for.

Building your nest egg

Adding to your superannuation is one of the most powerful and tax-effective ways to build your wealth over the long term. If you’re an employee, consider salary sacrifice to add to the mandatory contributions made by your employer. Even a small amount, paid regularly, will make a big difference over time. Don’t forget that there are some limits on how much you can invest before tax is affected, so it’s a good idea to keep track of any before-tax, or concessional, contributions.i

Small business owners, sometimes struggling with cash flow issues, may be tempted to neglect their own super contributions but you risk missing out on the benefits later in life.

Finding ways to cut living expenses and reducing or eliminating debt, including paying off the mortgage as quickly as possible, are also obvious ways to attain financial security, although not always easy to implement with cost-of-living pressures. But, again, any small and regular steps towards your goal are a positive contribution.

Preparing for the unexpected

Apart from finding ways to build your wealth and reducing debt, being prepared for unexpected losses is another way to secure your future.

For example, losing your home, business premises or vehicle in a catastrophic event when you’re not adequately insured creates a significant financial burden.

As natural catastrophes increase in frequency and intensity so does the ‘protection gap’, the economic losses caused by underinsurance or no insurance. One study estimated these losses in Australia at more than $18 billion in the nine years to 2023.ii

The Insurance Council of Australia (ICA) says there are some common reasons for underinsurance.iii

Making an incorrect guess about how much it would cost to repair, rebuild or replace property and contents. The ICA suggests using a building insurance calculator and a contents insurance calculator. Most insurers include both types of calculators on their websites.

Forgetting to update your insurance after upgrades to your home and belongings. Renovations, new furniture, and upgraded appliances can all add to the value of your home. It’s a good idea to reconsider the value of replacement at least every time you renew your policy.

Adding the extra costs such as demolition, clean-up, asbestos removal, council applications, architect, and surveyor services, and even the cost of temporary accommodation during a rebuild.

Not accounting for all your assets – you probably own a lot more than you realise. Have you included the contents of your garden shed and you wardrobe?

Financial protection for personal events

Protecting yourself financially against unexpected personal events is also worth weighing up.

A survey of more than 5000 working Australians shows that, on average, almost 80 per cent have car insurance while just one-third have life insurance.iv

Life insurance is a valuable protection for your family if something happens to you. There is also income protection insurance and various other personal insurances that can ensure you continue to receive an income when you’re unable to work.

While cost-of-living pressures might make insurance or self-insurance seem like a luxury you can’t afford, making an informed choice is the best you can do. That means the financial risks associated with events that affect yourself or your property and carefully weighing your options.

We’d be happy to help you review your wealth building and risk strategies and solutions for a financially safer 2025 and beyond.

The many unpredictable events of 2024 could easily have been disastrous for investment markets. Instead, we saw remarkable resilience and growth despite occasional volatility as investors reacted to the extraordinary times.

While economic growth in Australia and overseas was underwhelming, share markets rode out the ups and downs to finish 2024 strongly. 2024 was the ‘super election year’, when almost 2.5 billion people in 70 countries voted.i One result that has captured the attention of governments and analysts around the world is Donald Trump’s return to office in the United States. He has promised massive tariffs, tax cuts and increased spending on defence. All measures are likely to increase inflation and budget deficits which will affect global markets and economies.ii

Continuing geopolitical upheaval also marked the year. Tension in the Middle East grew as Israel expanded its campaign and European Union economies came under increased pressure when Ukraine stopped the flow of Russian gas.

The US dollar ended the year on a two-year high but that, and a weakening Chinese Yuan, led to a two-year low for the Australian dollar, which ended the year just below 62 US cents.iii

Cost of living falls but interest rates steady

Around the world, interest rates fell during the year but in Australia, after five interest rate increases in 2023, the Reserve Bank (RBA) held steady at 4.35 per cent, believing inflation is still too high.

Nonetheless, the cost of living has fallen significantly, down to 2.8 per cent in the September quarter from a high of 7.8 per cent two years ago and 3.8 per cent in the June quarter.iv

Falls in electricity and petrol prices contributed to the easing.

Australia’s economy grew by 0.8 per cent in the three quarters to the end of September – it’s slowest in decades.v

House prices mixed across the country

The housing market appeared to cool by the end of the year with average national home values falling by 0.1 per cent in December to a median of $815,000.vi

CoreLogic’s Home Value Index data shows four of the eight capitals recording a decline in values between July and December. These included Melbourne, Sydney, Hobart and Canberra. While in Perth, Brisbane, Adelaide and Darwin, home values increased.

Share markets survive and prosper

Global share markets were unsinkable in a year of stormy economic and political conditions.

The Nasdaq surged more than 30 per cent for the year. The S&P 500 was up 25 per cent – pushed along by the ‘magnificent seven’ tech stocks – and the Dow rose 14 per cent.

Although not quite in the same league, the ASX performed strongly, recording 24 new record highs during 2024. The S&P/ASX 200 closed the year at 8159, up 7.5 per cent, with some analysts predicting 2025 will close around 8800.

Commodities

Gold came into its own as a safe haven for those concerned about events around the globe, reaching an all-time high in October and adding more than 28 per cent for the year.

Oil prices were subdued with investors cautious about a glut, the risks of wider conflict in the Middle East, the war in Ukraine and the change of government in the US. Although there is some optimism for improved growth in China in 2025.

Iron ore prices have continued to decline, now down to about half of the peak US$200 a tonne in 2021.

Looking ahead

Economists’ forecasts vary on the timing of a cut in interest rates in 2025 but some believe there will be as many as four cuts, reducing the rate to 3.35 per cent by year end.

Share price volatility is expected to continue as investors roll with the global political and economic punches and the upcoming Australian Federal Election is likely to introduce uncertainty until the results are in.

If you’d like to review your goals for the coming year in the light of recent and expected developments, don’t hesitate to get in touch.

At this time of year, when giving is particularly on our minds, some might turn their attention to how best share their wealth or an unexpected windfall with their loved ones.

You might be thinking about handing over a lump sum to help them with a major purchase or business opportunity, or be keen to help reduce or extinguish their student loans. Alternatively, it might be about helping to solve a housing problem.

Whatever the reason there are some rules that it is worth being aware of to ensure both you and they are protected.

Giving a cash gift

You can give anyone, family or not, a gift of cash for any amount and, as long as you don’t materially benefit from the gift or expect anything in return, no tax is paid on the amount by either you or the receiver.i

The same applies if you’re planning to pay out your child’s student loans.

However, be aware that if the beneficiary of your cash gift is receiving a government benefit, such as an unemployment benefit or a student allowance, there is a limit on the size of the gift they can receive without it affecting their payments.

They may receive up to $10,000 in one financial year or $30,000 over five financial years (which can not include more than $10,000 in one financial year).ii

Helping out with housing

Many parents also like to help their children get into the property market, where possible.

It’s been a difficult time for many in the past few years in dealing with the COVID-19 pandemic, the rising cost of living and interest rates, and a housing crisis.

A Productivity Commission report released this year found that while most people born between 1976 and 1982 earn more than their parents did at a similar age, income growth is slower for those born after 1990.iii

With money tight and house prices climbing, three in five renters don’t believe they will ever own a home even though most (78 per cent) want to be homeowners, according data collected by the Australian Housing and Urban Research Institute (AHURI).iv

Just over half of those surveyed (52 per cent) were renting because they didn’t have enough for a home deposit and 42 per cent said they couldn’t afford to buy anything appropriate, the AHURI survey found.

So, in this climate, help from parents to buy a home isn’t just a nice-to-have, it’s becoming a necessity for many.

Moving home

Allowing your adult child, perhaps with a partner and family, to share the family home rent-free is common option, giving them the chance to save up for a deposit.

One Australian survey found that one-in-10 people had moved back in with their parents either to save money or because they could no longer afford to rent.v

If it gets too much living under the same roof, building a granny flat in your backyard may be an option. Of course there are council regulations to consider, permits to be obtained and the cost of building or buying a kit but on the upside, it may add value to your home.

Becoming a guarantor

Another way to help might be to become a guarantor on your child’s mortgage. This might be the best way into a mortgage for many but before you sign, think it through carefully, understand the loan contract and know the risks.vi

Don’t forget that, as guarantor, you’re responsible for the debt. You will have to step in and repay if the borrower can’t afford to repay, and the loan will be listed as a default on your own credit report.

Any sign that you are being pressured to be a guarantor on a loan may be a sign of financial abuse. There are a number of avenues for advice and support if you’re concerned.

It’s vital that you obtain independent legal advice before signing any loan documents.

If you would like more information about how to provide meaningful financial support to your children, we’d be happy to help.

Ah, Christmas! – the time of year when your bank account shrinks, your social calendar explodes, and your family dynamics resemble a poorly scripted soap opera. As we navigate this festive minefield of shopping, social gatherings, and feasting, it’s common to feel a little frazzled.

In fact, research has found that the holiday season is one of the six most stressful life events we go through, in the same category as moving house and divorce.i

But it does not have to be – before you let the silly season get the better of you, here are some ways to not just survive, but thrive, to make it through the festive chaos and bring in 2025 feeling energised and on track to reaching your goals.

Get organised

Let’s face it, the silly season is a whirlwind. Between work parties, family catch-ups, and obligatory gatherings with distant relatives you only see once a year, it’s enough to make anyone want to retreat to a deserted island.

However, rather than running off to Bora Bora, if you want to survive the silly season relatively unscathed, planning ahead is a must. With the social calendar filling up quicker than you can say cheers, it becomes easy to overcommit and leave yourself feeling a little stretched. Rather than maintaining a constant schedule of parties and social engagements, why not learn the power of saying ‘no’. Choose the events you really want to attend and think about each invitation before you send that RSVP. Remember to allow for some guilt-free ‘down time’ amongst all the festivities.

Shopping shenanigans

Shopping during the silly season can be akin to a scene from an action movie—chaotic, frenzied, and with a distinct chance of an all-in brawl.

Channel your inner Santa Claus and make a list. And yes, check it twice! A good list keeps you focused and reduces the chances of impulse buys—like that life-sized inflatable Santa that seemed like a good idea at the time. (Spoiler alert: it wasn’t.)

Consider shopping online, too. You can sip your coffee in your pyjamas while avoiding the chaos of the shops. Just remember: the delivery cut-off dates are real! Don’t be the person frantically searching for gifts at 9 PM on Christmas Eve.

The present predicament

Let’s talk presents. It’s lovely to give and receive gifts, but when did we all agree that every adult needs a new mug or another pair of socks?

To combat the gift-giving madness, consider doing a Secret Santa among adults. Set a reasonable budget and unleash your creativity. Who doesn’t want a mysterious gift that could range from a novelty toilet brush to a box of chocolates?

Navigating the family dynamics

Family gatherings can be a delightful mix of love, laughter, and the occasional argument that would make for great reality TV. You know the drill—everyone has an opinion, and even the Christmas ham can become a hot topic of debate.

Before the big day, set some ground rules. No politics, no discussing that relative’s questionable life choices, and absolutely no karaoke unless everyone is fully prepared to participate. If tensions start to rise, a little humour can go a long way. Embrace the absurdity of it all. If Uncle Bob starts arguing about the best way to cook prawns, counter with a story about how Auntie Sheila once tried to deep-fry a turkey—because that’s a Christmas classic in its own right.

Don’t try to do it all

If you’re hosting this year, congratulations! You’re officially in charge of managing the chaos. But you don’t have to shoulder the entire load.

Encourage those who are coming to bring their ‘special’ dish. Not only does it lighten your load, but it also allows everyone to show off their culinary skills (or lack thereof). Plus, you might discover that Aunt Margaret’s “special” potato salad is actually a hidden gem—just don’t ask what’s in it.

Survive and thrive

At the end of the day embrace the chaos, lean into the hilarity of when things don’t go to plan, don’t take it all too seriously and be prepared to step back a little when you need a break from all the festivities.

Here’s to a joyful festive season filled with laughter and the wonderful chaos that is Christmas. We’ll catch you on the other side. Cheers!

Self managed super funds (SMSFs) can offer their members many benefits, but one that’s often overlooked is their potential as a multigenerational wealth creation and transfer vehicle.

Family SMSFs are relatively rare. According to the most recent ATO statistics (2022-23), the majority of SMSFs (93.2 per cent) have only one or two members.i Just 6.6 per cent have three or four members and only 0.3 per cent have five or six members (the maximum allowed).

Advantages of a family SMSF

An SMSF is sometimes established when two or more generations of a family share ownership or work in a family business. The fund can then form part of a personal and business succession plan, potentially making it easier to pass on ownership and management of assets to the next generation.

With more members, SMSFs also gain additional scale, allowing them to invest in larger assets (such as property). You can add business premises to the SMSF and lease it back without violating the related parties rule and 5 per cent limit on in-house assets.ii

Reduced tax and administration costs are also a benefit of multigenerational funds.

Running a family SMSF means the costs of establishing and administering the fund are spread across more members. This can be particularly helpful for adult children just beginning to save for their retirement.

In addition, more fund members means more people to share the administrative burdens of running an SMSF, which may be helpful as you get older.

A family SMSF does not need to be automatically wound up if you die or lose mental capacity and they can simplify the process of paying out a member death benefit as well as potentially allowing it to be paid tax-effectively. Note that death benefits paid to non‑tax dependent beneficiaries incur a tax rate of up to 30 per cent plus the Medicare levy.iii

More fund members also make setting up a limited recourse borrowing arrangement (LRBA) easier because their contributions reduce the fund’s risk of being unable to pay the borrowing costs. (An LRBA allows an SMSF to borrow money to buy assets)

Funding pension payments

Another advantage of an SMSF with up to six members may be when the fund begins making pension payments to older members.

If younger members are still making regular contributions, fund assets don’t need to be sold to make pension payments, which avoids the realisation of capital gains on assets.

Family SMSFs can also provide non-financial benefits, helping to transfer financial knowledge and expertise between the generations. And, while your children gain a solid financial education from participating in the running the SMSF, they can also provide valuable investment insights from a different perspective.

Risks and responsibilities

It is important to note that a multigenerational SMSF may not be right for everyone.

SMSFs of any size come with some risks and responsibilities. You are personally liable for the fund’s decisions, even if you act on advice from a professional, and your investments may not provide the returns you were hoping for.

Before you start adding your children and their spouses to your fund, it’s essential to spend time thinking about the challenges in running a family SMSF. Developing an asset allocation strategy catering to different life stages can be complex. Older members may prefer a strategy designed to deliver a consistent income stream, while younger members are usually more focused on capital growth.

Risk profiles are also likely to vary. Typically, younger fund members have a higher appetite for investment risk than members closer to retirement.

Family conflict can also be an issue when relationships are under pressure from divorce, blended families, and personality clashes.

The death of a parent can also create disputes over the distribution of fund assets or forced asset sales. Decisions about the payment of death benefits by the remaining trustees can derail carefully made estate plans and result in expensive legal battles.

Larger families with multiple adult children and partners may also find the six member limit an obstacle, forcing them to look at other options such as running a number of family SMSFs in parallel.

If you would look more information about establishing a family SMSF, call our office today.

There is no debate that Australians love investing in property. The value of Australian residential real estate at the end of August 2024 was an estimated $10.95 trillion.i

Some love it so much that they believe property is a better option for providing a retirement income. They see a bricks and mortar investment as a more tangible and solid approach than say, superannuation, preferring to take their super as a lump sum on retirement to buy property. They may also choose to invest a windfall, such as an inheritance, or the proceeds from downsizing the family home, in property instead of their super.

So, given that a retired couple above age 65 needs an estimated yearly income $73,337 to lead a comfortable lifestyle, could a property investment do the job?ii

While it’s true that a sizeable property portfolio could deliver rental income to equal a super pension, it might mean missing out on some useful benefits.

After all, super is a retirement savings structure with significant tax advantages. It also has the flexibility to provide investments in a range of different asset classes, including property.

Meanwhile, super fund performance has, generally speaking, outstripped house price movements over the past decade. Super funds (invested in an all-growth category) returned an annual average of 9.1 per cent during that time while average house prices in Australian capital cities grew 6.5 per cent per year over the same period.iii, iv

Not that past performance can give you any guarantees about what will happen in the future. Indeed, the average numbers smooth out the years of high returns and the years of negative returns. More important considerations in making an informed decision are your financial goals, your investment timeframe and how much risk you’re comfortable with.

Liquidity

One of the most significant differences between super and property investments is liquidity, or how quickly you can convert your investment to cash.

With super, assuming you’re eligible, funds can be accessed relatively easily and quickly. On the other hand, if your wealth is tied up in property it may take some time to sell or it may sell at a lower price.

Nonetheless, market cycles affect both property and super investments. They can be affected by volatile conditions and deliver negative returns just at the time you need access to a lump sum.

Long-term investing

Superannuation is designed for long-term growth, often spanning decades as you accumulate wealth over your working life. The magic of compounding interest can lead to substantial growth over time, depending on your investment options and the state of the market.

Property investments, on the other hand, can be invested for short, medium, and long-term growth depending on the suburb, the street, and the type of house you invest in. Of course, there are additional costs in buying a property (such as stamp duty) plus costs in selling (including capital gains tax). If there’s a mortgage over the property, you’ll need to factor in the additional costs of repayments and interest (bearing in mind that interest on investment properties is tax deductible).

Risk appetite

Investors’ attitudes towards risk also play a role in choosing between super and property.

Superannuation funds can be diversified across various asset classes, which helps to reduce risk. But property investments expose investors to a single market meaning that while there might be a big benefit from an upswing, any downturn may be a blow to a portfolio.

Making an informed choice

Ultimately, any decision between superannuation and property should align with individual financial goals, risk tolerance, and investment strategies. And, of course, it doesn’t need to be one or the other – many choose to rely on their super while also holding investment property so it’s best to understand how super and property can complement each other in a well-rounded retirement plan.

We’d be happy to help you analyse your retirement income strategy to develop a plan that works for you.