RGM are proud to announce that financial advisory firm Money Talk Planners will be joining forces with RGM come the 1st of July 2025.

Money Talk Planners is a locally, family-owned financial planning business based out of Morwell that has been in operation for over 30 years. It has a reputation of providing high quality advice to its clients in a professional manner; values that underpin the services we provide at RGM. With the move, the entire Money Talk Planners team will reside in our Traralgon office.

There will be no change to the existing service provided to all our financial planning and accounting clients. Joe Auciello, Partner of over ten years in both our accounting and financial planning divisions, explains why RGM sought out this alliance. “In the ever-growing financial advisory sector, it is imperative that as a business, we look at strategic moves to ensure we can bolster our service offering to existing and new clientele. The Money Talk Planners team will bring their own ideas across to RGM that we look forward to incorporating into our business. Over the past two years we have been diligently working in the background to ensure that this move puts RGM at the forefront of financial planning in Gippsland both now and into the future”.

As part of the move, MTP practice principal Tony Salvatore and financial advisor Adrian Salvatore will join the ownership group of RGM. With over 30 years of financial of financial planning experience, Tony is excited about the move. “Both businesses have shared values, and we will be able to offer enhanced resources, greater financial guidance and invest quality time with our clients. It will be business as usual.”

We formally welcome the Money Talk Planning team across to RGM and we’re all excited in what the future holds!

The number of Australians aged over 65 is expected to more than double in the next 40 years while the number of people aged over 85 is predicted to triple in that time.i

Aged care funding and services have seen major changes in the years since the 2021 report of the Royal Commission into Aged Care Quality and Safety, and this year is no exception.

1 July 2025 marks the start of a host of new programs and improvements for the aged care sector. Several announcements have already been made this year, covering wage rises for aged care workers and nurses, and an increase in government funding for residential aged care accommodation.

In one of the most significant changes, the new Aged Care Act begins on 1 July. The Act aims to ensure the viability and quality of aged care.

A report by the Aged Care Taskforce last year calculated the residential aged care sector will need $56 billion by 2050 to upgrade facilities and build more rooms.

Current funding arrangements aren’t working. In the 2022-2023 financial year, almost half of all accommodation providers made a loss.

Some $300 million in federal grants will be delivered to accommodation providers this year to help with capital works upgrades.

And to improve the viability of the facilities the government is introducing other measures including larger means-tested contributions from new entrants and a higher maximum room price that is indexed over time.

Aged Care Minister Anika Wells says half of new residents will not contribute more under the new consumer contributions.

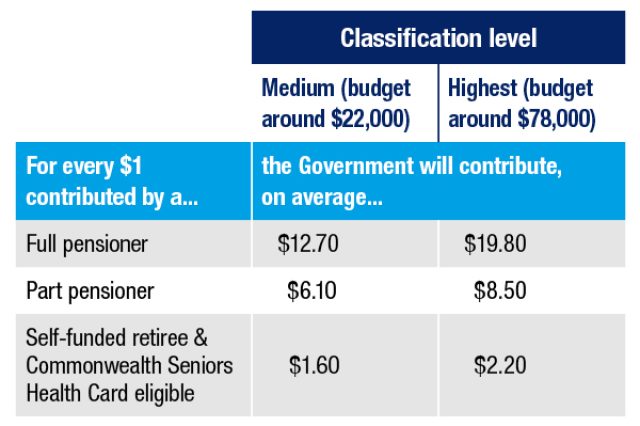

“For every $1 an older Australian contributes to their residential aged care, the government will contribute an average of $3.30,” says Wells.

Support at Home

The Aged Care Act also aims to support more people who want to stay in their own homes as they age. The federal government is investing $4.3 billion in a new Support at Home program, which replaces the Home Care Packages and the Short-Term Restorative Care programs.ii

There’ll be more than 300,000 places available over the next 10 years and a shorter waiting period for Support at Home, and there’s a goal to simplify and improve the assessment process, making it easier to access different services as needs change.iii

Similar to the Home Care Package, Support at Home will provide:

clinical care, such as nursing and occupational therapy,

help with maintaining independence including showering, dressing and taking medications, and

support for everyday living tasks such as cleaning, gardening, shopping and meal preparation.

The government will pay 100 per cent of clinical care costs while Support at Home recipients will make a contribution towards independence and everyday living costs. The contribution amount will be calculated using the Age Pension means test and it depends on the level of support needed and the combination of income and assets. The highest classification with the most funding will receive a package of services worth $78,000 per year. There’ll also be funding for assistive technology and home modifications and end of life care.

A new cap on contributions will also apply. No one will pay more than $130,000 in their lifetime – whatever their means or length of care at home or in residential accommodation.

Refunding deposits

The new Aged Care Act also requires aged care accommodation providers to refund residents’ lump sum deposits within 14 days if they move to another facility or pass away. Interest must be paid on the lump sum until the amount is repaid. As before, some deductions are permitted provided they were included in the original agreement.

No disadvantage

For those already receiving home care packages or in aged care accommodation, the government says a ‘no-worse-off’ principle will provide certainty that they won’t have to pay more under the new laws.

Whether it is you or a loved one who is considering moving into aged care, it can be an emotional time. With these new changes being implemented, you may have a few questions. Please give us a call if you’d like to hear more about the changes or if we can help to assess your next step or plan ahead.

In the shadow of an upcoming election, Jim Chalmers’ fourth Budget delivered small but unexpected tax cuts for all Australian taxpayers.

The modest cuts were delivered against a backdrop of growing economic uncertainty, with the treasurer emphasising the need for national resilience in the face of rapid global change.

Tax cuts for everyone

In a surprise revelation, the treasurer announced two new tax cuts in the 2025 Budget.

The first is a cut in the lowest personal income tax rate, which covers every dollar of a taxpayer’s income between $18,201 and $45,000. The current 16 per cent rate will reduce to 15 per cent in 2026-27 and be lowered again to 14 per cent from 1 July 2027.

According to the government, the reduction will take the first tax rate down to its lowest level in more than half a century. Combined with the 2024 tax cuts, an average earner will be paying $2,190 less in 2027-28 compared with 2023-24.

The second tax cut is an increase of 4.7 per cent to the Medicare low-income threshold for singles and families. This means the Medicare Levy will not kick in until singles earn $27,222, rather than the current $26,000 level. The threshold for families will rise from $43,846 to $45,907, while single seniors and pensioners will have their threshold increase from $41,089 to $43,020.

Energy relief for small business and households

The Budget also provided small businesses and households with a welcome additional energy bill rebate to cope with the burden of high energy costs.

Around one million eligible small businesses will receive an additional $150 directly off their energy bills from 1 July 2025. This will extend the government’s energy bill relief until the end of 2025, as the previous rebate scheme was due to end on 30 June.

Abolition of non-compete clauses and licensing reform

Some businesses may be less pleased with the Budget announcement of a planned ban on non-compete clauses covering low- and middle-income employees leaving for another business or to start their own.

Competition law will be tightened to prevent businesses making arrangements that cap workers’ pay and conditions without their knowledge or agreement, or that block them from being hired by competitors. The government claims this will increase affected employees’ wages by up to 4 per cent as they will be able to move to more productive, higher-paying jobs.

Work will also begin on a national occupational licence for electrical trades, which is intended to provide a template for other industries where employees are currently restricted from working across state and territory borders.

Beer excise freeze

Government support for the hospitality sector and alcohol producers was also announced in the Budget.

Indexation of the draught beer excise and excise equivalent customs duty rates will be paused in a measure costing about $165 million over five years.

Strengthening competition law

Small business will benefit from the government’s decision to work with the states and territories to extending unfair trading practices protections to small businesses.

Over $7 million will be provided over two years to strengthen the Australian Competition and Consumer Commission’s enforcement of the Franchising Code.

Subject to consultation, protections from unfair contract terms and unfair trading practices will be extended to all businesses regulated by the Franchising Code.

Supporting Australian businesses

Local companies will also benefit from $20 million in additional support for the Buy Australian Campaign, which encourages consumers to buy Australian-made products.

The Budget further supported local businesses with $16 million in funding for a new Australia-India Trade and Investment Accelerator Fund.

Additional ATO tax compliance funding

The ATO will be happy, with the 2025 Budget providing $999 million over the next four years to extend and expand its tax compliance activities.

This includes additional funding for the shadow economy and personal income tax compliance programs, together with $50 million from 1 July 2026 to ensure the timely payment of tax and unpaid super liabilities by businesses and wealthy groups.

Preparing for the Fringe Benefits Tax (FBT) year-end is never a walk in the park and, with the ATO now using increasingly sophisticated data matching programs, it is more important than ever to get your return right.

As part of the ATO’s post-pandemic campaign to improve taxpayer compliance and payment of tax debts, the ATO is using data matching tools to check whether businesses should be reporting employee fringe benefits and paying tax on them.i

As a small business owner, you shoulder full responsibility for accurately calculating the taxable value of all fringe benefits, lodging the FBT return, paying any required tax, and reporting fringe benefits on an employee’s payment summary if the individual benefits exceed $2,000.ii

Areas to check in your FBT return

Vehicle benefits are a continuing source of mistakes when it comes to FBT returns. The ATO is particularly interested in commercial vehicles (mainly dual cab utes) provided to employees. Many employers wrongly believe these vehicles are fully FBT-exempt. But an exemption only applies where private use of the vehicle is minor and infrequent.

FBT rules about the use of employee car parking have also been tightened. FBT usually applies if you provide your employees with parking in a commercial car park, although many small businesses are eligible for an FBT exemption under specific conditions.iii

Dining and EV benefit rules

Entertainment and in-house dining fringe benefits are another area where it’s easy to be caught out.

Ensure you have detailed records related to these types of benefits (including any contributions made by employees) and check the benefits provided have met the ‘minor and infrequent‘ rule.

Also keep an eye on the implications of new rules covering electric vehicle (EV) benefits.

Getting employees to play their part

To simplify the process of putting your FBT return together, it helps if your employees play their part.

For example, encourage employees who use salary packaging to spend all of their available annual balance before 31 March to avoid the headache of unspent or claimed benefits rolling over into the next FBT year.

If employees do not use their unspent balance, it still needs to be reported and deducted from their cap limit in the new FBT year, which can create additional paperwork.

Employee declarations

If you plan to use the FBT exemptions and concessions on offer, you may also need to obtain detailed records from your employees (such as travel diaries, logbooks, declarations and odometer records).iv

Any change in car usage due to a new work role needs to be noted and the business use percentage adjusted, or a new logbook started.

Start collating this information as early as possible to simplify the calculation and lodgement process.

Meeting the lodgement deadline

Unlike the normal tax year, the FBT year ends on 31 March, with the 21 May lodgement and payment deadline giving you only a short window to get your paperwork in order. If you lodge with an accountant the deadline is 25 June.

You need to determine the taxable value of the different fringe benefits your employees have received during the year, calculate the tax you need to pay and collect any required employee declarations.

All employee declarations must be obtained by the time your FBT return is due to be lodged. Even if you do not have to lodge a return, you must have the declarations by 21 May.

We can help with any questions you may have and assist you with preparing your FBT return.

At this time of year, when giving is particularly on our minds, some might turn their attention to how best share their wealth or an unexpected windfall with their loved ones.

You might be thinking about handing over a lump sum to help them with a major purchase or business opportunity, or be keen to help reduce or extinguish their student loans. Alternatively, it might be about helping to solve a housing problem.

Whatever the reason there are some rules that it is worth being aware of to ensure both you and they are protected.

Giving a cash gift

You can give anyone, family or not, a gift of cash for any amount and, as long as you don’t materially benefit from the gift or expect anything in return, no tax is paid on the amount by either you or the receiver.i

The same applies if you’re planning to pay out your child’s student loans.

However, be aware that if the beneficiary of your cash gift is receiving a government benefit, such as an unemployment benefit or a student allowance, there is a limit on the size of the gift they can receive without it affecting their payments.

They may receive up to $10,000 in one financial year or $30,000 over five financial years (which can not include more than $10,000 in one financial year).ii

Helping out with housing

Many parents also like to help their children get into the property market, where possible.

It’s been a difficult time for many in the past few years in dealing with the COVID-19 pandemic, the rising cost of living and interest rates, and a housing crisis.

A Productivity Commission report released this year found that while most people born between 1976 and 1982 earn more than their parents did at a similar age, income growth is slower for those born after 1990.iii

With money tight and house prices climbing, three in five renters don’t believe they will ever own a home even though most (78 per cent) want to be homeowners, according data collected by the Australian Housing and Urban Research Institute (AHURI).iv

Just over half of those surveyed (52 per cent) were renting because they didn’t have enough for a home deposit and 42 per cent said they couldn’t afford to buy anything appropriate, the AHURI survey found.

So, in this climate, help from parents to buy a home isn’t just a nice-to-have, it’s becoming a necessity for many.

Moving home

Allowing your adult child, perhaps with a partner and family, to share the family home rent-free is common option, giving them the chance to save up for a deposit.

One Australian survey found that one-in-10 people had moved back in with their parents either to save money or because they could no longer afford to rent.v

If it gets too much living under the same roof, building a granny flat in your backyard may be an option. Of course there are council regulations to consider, permits to be obtained and the cost of building or buying a kit but on the upside, it may add value to your home.

Becoming a guarantor

Another way to help might be to become a guarantor on your child’s mortgage. This might be the best way into a mortgage for many but before you sign, think it through carefully, understand the loan contract and know the risks.vi

Don’t forget that, as guarantor, you’re responsible for the debt. You will have to step in and repay if the borrower can’t afford to repay, and the loan will be listed as a default on your own credit report.

Any sign that you are being pressured to be a guarantor on a loan may be a sign of financial abuse. There are a number of avenues for advice and support if you’re concerned.

It’s vital that you obtain independent legal advice before signing any loan documents.

If you would like more information about how to provide meaningful financial support to your children, we’d be happy to help.

Ah, Christmas! – the time of year when your bank account shrinks, your social calendar explodes, and your family dynamics resemble a poorly scripted soap opera. As we navigate this festive minefield of shopping, social gatherings, and feasting, it’s common to feel a little frazzled.

In fact, research has found that the holiday season is one of the six most stressful life events we go through, in the same category as moving house and divorce.i

But it does not have to be – before you let the silly season get the better of you, here are some ways to not just survive, but thrive, to make it through the festive chaos and bring in 2025 feeling energised and on track to reaching your goals.

Get organised

Let’s face it, the silly season is a whirlwind. Between work parties, family catch-ups, and obligatory gatherings with distant relatives you only see once a year, it’s enough to make anyone want to retreat to a deserted island.

However, rather than running off to Bora Bora, if you want to survive the silly season relatively unscathed, planning ahead is a must. With the social calendar filling up quicker than you can say cheers, it becomes easy to overcommit and leave yourself feeling a little stretched. Rather than maintaining a constant schedule of parties and social engagements, why not learn the power of saying ‘no’. Choose the events you really want to attend and think about each invitation before you send that RSVP. Remember to allow for some guilt-free ‘down time’ amongst all the festivities.

Shopping shenanigans

Shopping during the silly season can be akin to a scene from an action movie—chaotic, frenzied, and with a distinct chance of an all-in brawl.

Channel your inner Santa Claus and make a list. And yes, check it twice! A good list keeps you focused and reduces the chances of impulse buys—like that life-sized inflatable Santa that seemed like a good idea at the time. (Spoiler alert: it wasn’t.)

Consider shopping online, too. You can sip your coffee in your pyjamas while avoiding the chaos of the shops. Just remember: the delivery cut-off dates are real! Don’t be the person frantically searching for gifts at 9 PM on Christmas Eve.

The present predicament

Let’s talk presents. It’s lovely to give and receive gifts, but when did we all agree that every adult needs a new mug or another pair of socks?

To combat the gift-giving madness, consider doing a Secret Santa among adults. Set a reasonable budget and unleash your creativity. Who doesn’t want a mysterious gift that could range from a novelty toilet brush to a box of chocolates?

Navigating the family dynamics

Family gatherings can be a delightful mix of love, laughter, and the occasional argument that would make for great reality TV. You know the drill—everyone has an opinion, and even the Christmas ham can become a hot topic of debate.

Before the big day, set some ground rules. No politics, no discussing that relative’s questionable life choices, and absolutely no karaoke unless everyone is fully prepared to participate. If tensions start to rise, a little humour can go a long way. Embrace the absurdity of it all. If Uncle Bob starts arguing about the best way to cook prawns, counter with a story about how Auntie Sheila once tried to deep-fry a turkey—because that’s a Christmas classic in its own right.

Don’t try to do it all

If you’re hosting this year, congratulations! You’re officially in charge of managing the chaos. But you don’t have to shoulder the entire load.

Encourage those who are coming to bring their ‘special’ dish. Not only does it lighten your load, but it also allows everyone to show off their culinary skills (or lack thereof). Plus, you might discover that Aunt Margaret’s “special” potato salad is actually a hidden gem—just don’t ask what’s in it.

Survive and thrive

At the end of the day embrace the chaos, lean into the hilarity of when things don’t go to plan, don’t take it all too seriously and be prepared to step back a little when you need a break from all the festivities.

Here’s to a joyful festive season filled with laughter and the wonderful chaos that is Christmas. We’ll catch you on the other side. Cheers!

On Friday the 18th of November I set out to run 100km around the local Yarragon Football oval to help raise awareness and funds for Neuroblastoma, a cancer affecting young children of which on average are just 2 years of age,

Our family has been affected by this terrible cancer with my nephew being diagnosed with stage 4 Neuroblastoma at 8 weeks old, thankfully he has been in remission for two years.

Throughout the day 20-30 people took part running lap after lap in the rain and many PB’s were achieved which made the km’s tick over much quicker,

My nephew and his brother were able to come along for the final few laps to run them with me,

Almost $3,000 was raised to add to Paddy’s tally by the end of the run.

If you are feeling a bit like the meat in the sandwich you are not alone. The ‘sandwich generation’ is a growing social phenomenon that impacts people from all walks of life, describing those at a stage of their lives where they are caring for their offspring as well as their elderly parents.

The phenomenon is gathering momentum as we are tending to live longer and have kids later. It even encompasses royalty – Prince William has been dealing with a sick father while juggling school aged kids (as well as a partner dealing with serious health issues).

A growing phenomenon

The number of people forming part of the sandwich generation has grown since the term was first coined in the 1980’s, as we tend to live longer and have kids later. It is estimated that as many as 5% of Australians are currently juggling caring responsibilities which has implications for family dynamics, incomes, retirement and even the economy.i

Like many other countries, the number of older Australians is growing both in number and as a percentage of the population. By 2026, more than 22 percent of Australians will be aged over 65 – up from 16 percent in 2020.ii It is also becoming more common for aging parents to rely on their adult children for assistance when living independently becomes challenging.

The other piece of bread in the sandwich is that as a society we are caring for kids later in life. The median age of all women giving birth increased by three years over two decades.iii

And with young people staying in the family home well into their twenties, we are certainly supporting our children for longer. Even after the kids leave the nest, it’s also common for parents to become involved in looking after grandchildren.

Taking its toll on carers

While we want to support our loved ones, when that support is required constantly and intensively for both parts of the family, it can mean that something has to give and that ‘something’ is often the carer’s well-being.

Even if you are not part of the sandwich generation but being squeezed at either end – caring for kids or parents, acting as a primary care-giver often requires you to provide physical, emotional, and financial support. It’s common to feel it take a toll on your own emotional and physical health, and sometimes your finances as you sacrifice some of your savings or paid work to help your loved ones.

Support for caregivers

It can be difficult to acknowledge you need assistance but there are a number of ways you can access help.

Deciding what to get help with

It can feel like there is not enough hours in the day and that’s overwhelming. Try to think about what you really need to do and where your time is best spent and consider if you can get assistance with tasks or duties you don’t have to do. This may mean outsourcing things like buying a healthy meal instead of cooking or getting a hand with gardening or lawn mowing.

Think about what others could assist with to lighten and share your load.

Accessing support

There are also support networks out there that exist to take off some of the pressure. Reach out to local support networks via Carers Australia for help identifying mainstream and community supports.

You or your loved ones may also be entitled to government support, under the National Disability Insurance Scheme (NDIS) or My Aged Care. These programs provide funding and resources to help pay for essential care; from domestic assistance with cleaning and cooking, to home modifications, to 24-hour care for those who require more support.

The importance of self-care

It’s vital to take some time out for yourself and make your own wellbeing a priority. Don’t feel that it’s selfish to take care of your own needs as that’s an essential part of being a carer. Resources like respite care and getting support when needed is an important gateway to self-care.

Managing your finances

Caregiving can put financial pressure on the whole household and has the potential to impact retirement savings. The assistance of a trusted professional can help, and we are here if you need a hand.

Raising kids as well as supporting parents to live their best lives as they age is becoming more common and can be a challenging time of life. While the act of caring is the ultimate act of kindness – the most important thing to remember is to be kind to yourself.

A catchy business name, a trustworthy brand and an engaging website or social media presence are all vital to any small business. But don’t underestimate the effect of the business structure.

Choosing whether to operate as a sole trader, company, partnership or trust depends on many factors including cost, the size of the business, whether you have dependants and family members to share income with, and the degree of financial or legal risk involved in running the business.

Sole trader

Many small operators start out as a sole trader, and some decide to continue with this structure.

On the positive side, it’s easy to set it up and, with fewer business reporting obligations, it’s cheaper to run than other business structures.

There are one or two considerations that, depending on your circumstances, could mean a sole trader structure doesn’t work for you.

One of these is the extent of your liability if things go wrong. When you’re a sole trader your liability is unlimited, meaning your assets are at risk in the case of legal action. Some businesses may consider their risk to be too low to warrant changing the business structure or they may choose to find an insurance product to provide some protection.

Tax is another consideration. Among other issues, as a sole trader, you’re liable to pay tax on all income received by the business and you can’t split profits or losses with family members.i

Partnership

Two or more people can form a business partnership and distribute business income among themselves.

Like a sole trader structure, a partnership structure can be slightly cheaper to operate because there are minimal reporting requirements.

All partners are liable for all the debts and obligations of the business although there are different types of partnerships that vary liability among the partners.

For tax purposes, each partner reports their share of the partnership income or loss in their own return and pays tax on any income. Partners cannot claim a deduction for any money they withdraw from the business. Amounts taken from a partnership are not considered wages for tax purposes.ii

Company

A company structure has a number of advantages over a sole trader or partnership structure, but it costs more to set up and operate and there are more reporting requirements.

A company is considered a separate legal entity and has its own tax and superannuation obligations, but company directors have a number of legal responsibilities.

Companies pay an annual fee to be registered with the Australian Securities and Investments Commission (ASIC) and they usually cost more to put together the necessary annual accounts and tax return.

On the plus side, you will be able to employ yourself and claim a tax deduction for your wages.

But be aware of the Personal Services Income (PSI) rules. If more than 50 per cent of the income of the business is produced by your personal exertion, it’s considered PSI and you will pay tax at your marginal rate, rather than the lower company tax rate. This rule affects taxpayers with any business structure.

Trust

A trust is the most expensive and complex business structure to operate but it might be the most appropriate for your needs.

There are some pluses and minuses so expert advice from your accountant and lawyer is crucial. You will need help to decide on the type of trust, to set up a formal trust deed and to carry out annual administrative tasks.

On the positive side, there may be tax advantages and there are some protections from financial and legal liability.

On the flip side, all income earned must be distributed to beneficiaries each year otherwise tax is paid at the highest marginal rate. Also, losses can’t be distributed to beneficiaries, it may be difficult to dissolve or change elements of a trust and it may be more difficult to borrow funds.

Ask for guidance

The importance of choosing the best business structure for your needs and understanding the regulatory requirements is crucial to the success of any small business. Check in with us for expert guidance.

Employers need to check that payroll systems reflect recent legislative changes, and the ATO is highlighting deduction opportunities available to some small businesses. Here’s your roundup of the latest tax news.

Updated employer obligations

The ATO is reminding employers to stay on top of legislative changes affecting payroll systems.

The Super Guarantee rate increased on 1 July 2024 to 11.5 per cent of ordinary times earnings, so all payments (starting with those for the July to September quarter) to super accounts for eligible workers must reflect the new rate.i

Individual income tax rate thresholds and tax tables changed also changed on 1 July 2024 so you may need to check calculations for your Pay As You Go Withholding obligations.

Claims for energy expenses

Many small business are eligible for a bonus 20 per cent tax deduction for new assets (or improvements to existing assets), that support more efficient energy usage.

The Small Business Energy Incentive applies to eligible assets first used or installed ready for use between 1 July 2023 and 30 June 2024.ii

Eligible expenditure for external training courses for employees incurred between 29 March 2022 and 30 June 2024 could also qualify for a 20 per cent bonus tax deduction from the Small Business Skills and Training Boost.iii

Pay less capital gains tax (CGT)

While a business can reduce capital gains made during a tax year by offsetting them with capital losses from the same or previous income years, not all capital losses are eligible.iv

Capital losses carried forward from previous years need to be used first, with losses from collectables (such as artwork and antiques) only permitted to be offset against capital gains from collectables.

Losses from personal use assets (such as boats or furniture), CGT exempt assets (such as cars and motorcycles), paying personal services income to yourself through an entity you set up, and leases producing income (such as commercial rental property), are ineligible as offsets.

Fuel tax credit rates change

Before claiming fuel tax credits in your next Business Activity Statement (BAS), check you are using the latest rates as they have changed twice in the new financial year.v

On 1 July 2024, the rate for heavy vehicles travelling on public roads changed due to an increase in the road user charge, with the rate altering again on 5 August 2024 due to a change in fuel excise indexation.

Different rates apply based on when you acquired fuel for your business’ use, so ensure you use the correct rate. If you are unsure, try the ATO’s online Fuel Tax Credit Calculator to work out the amount to report in your BAS.

Records essential for rental expense claims

Rental property investors without correct documentation to substantiate their expense deductions may find their claims declared invalid.vi

The ATO is warning investors they need all receipts, invoices and bank statements plus details of how deductions were calculated and apportioned for a valid claim.

Lodging a ‘nil’ BAS

While taxpayers registered for GST automatically receive a Business Activity Statement and are required to lodge and pay in full by the due date, businesses with nothing to report are still required to lodge.

If you have paused your business, you are required to lodge a ‘nil’ BAS by the due date either online or via the ATO’s automated phone service.vii