Tax update June 2025

ATO individual and business priorities

The Australian Tax Office will be cracking down on work-related expenses in personal tax returns this year after recently revealing some of the claims that have been submitted in the past.

The ATO is also reminding businesses of this year’s limit for the popular instant asset write-off and its ongoing focus on GST fraud.

Here’s a roundup of the latest tax news.

‘Wild’ deduction claims

The tax office caused some raised eyebrows with its revelations about ‘wild’ work-related expense claims made by some taxpayers, including a mechanic claiming an air fryer, TV, gaming console and microwave.i

Other claims deemed to be personal rather than work-related included a truck driver claiming swimwear so he could go for a swim when stopped for a break, and a fashion industry manager claiming over $10,000 in luxury-branded clothing that was purchased to wear to work functions.

This time the ATO says it intends to focus on common taxpayer errors, such as work-related expenses, working from home deductions, and income from multiple sources (including side hustles like ride sourcing services or selling services via an app).

Instant asset write-off limit

The ATO is reminding taxpayers who purchased business assets during the financial year that the instant asset write-off limit in 2024-25 is $20,000.ii

The instant write-off (which allows you to immediately deduct the business part of the cost of eligible assets) is available to businesses with an aggregate annual turnover of less than $10 million who use the simplified depreciation rules.iii

The full cost of eligible depreciating assets (both new and second-hand) costing less than $20,000 on a per asset basis, may qualify for the deduction.

Focus on business GST fraud continues

A Melbourne man has been sentenced to 2 years and 11 months’ imprisonment after obtaining over $390,000 in fraudulent GST refunds and attempting to obtain a further $330,000.

The sentence reflects the continued ATO focus on stamping out GST fraud, with the acting deputy commissioner Kath Anderson noting there were “no ifs, ands or buts here – if you don’t run a business, you don’t need an ABN and you cannot claim GST refunds”.

The ATO-led Serious Financial Crime Taskforce remains on the lookout for potentially fraudulent GST activities, with information sharing identifying businesses using complex financial arrangements (such as false invoicing, misaligned GST accounting methods and claims for fake purchases) to obtain larger GST refunds.

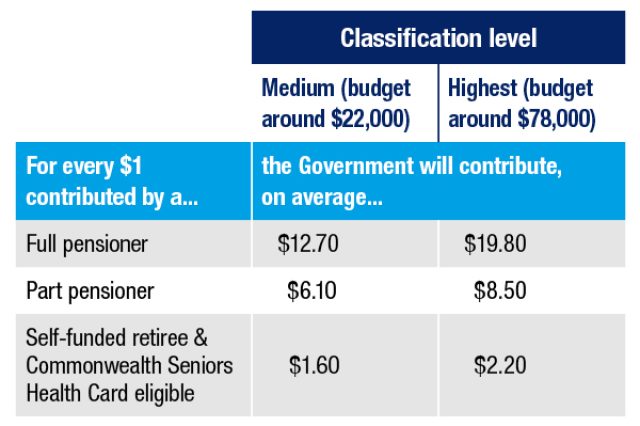

New small business benchmarks released

Small business owners keen to take the ‘pulse’ of their business can now use updated financial benchmarks covering 100 different industries produced by the ATO.

Updated annually, the benchmarks are designed to help business owners compare their performance against other businesses in the same industry.

Owners can use the information to identify if their performance is within the normal range for their industry, which mean it is less likely to attract ATO attention.iv

Paperless SMSF reporting

The ATO has emailed trustees of SMSFs still completing and lodging paper activity statements encouraging them to move to paperless reporting for improved security and convenience.

The regulator says benefits of paperless reporting include an additional two weeks on the fund’s lodgment deadline, reduced errors, faster refunds and easier recordkeeping.

In line with the push for greater digital SMSF reporting, the ATO recently noted non-lodgment of SMSF annual returns remains a concern and this can result in trustee penalties and removal of a fund’s compliance status.v

Estimates of illegal early access in SMSFs is also worrying the regulator, with prohibited loans from funds increasing.

Help with compromised TFNs

With identity theft continuing to increase, the ATO has updated its information for taxpayers who find their tax file number (TFN) has been compromised.

TFNs can be comprised through a number of different channels like email or phishing scams, or through data breaches at legitimate organisations as well as ID theft by criminals.

Anyone who believes their TFN has been compromised or used illegally should contact the ATO immediately on 1800 467 033.

i ATO unveils ‘wild’ tax deduction attempts and priorities for 2025 | Australian Taxation Office

ii Instant asset write-off for eligible businesses | Australian Taxation Office

iii Simpler depreciation rules for small business | Australian Taxation Office

iv ATO releases new small business benchmarks for 100 industries | Australian Taxation Office

v Highlights from the 2025 SMSFA conference | Australian Taxation Office